The insightful articles, inspiring narrations and analytical perspectives presented by the Editorial Team, establish an alluring connect with the reader. My compliments and best wishes to SP Guide Publications.

"Over the past 60 years, the growth of SP Guide Publications has mirrored the rising stature of Indian Navy. Its well-researched and informative magazines on Defence and Aerospace sector have served to shape an educated opinion of our military personnel, policy makers and the public alike. I wish SP's Publication team continued success, fair winds and following seas in all future endeavour!"

Since, its inception in 1964, SP Guide Publications has consistently demonstrated commitment to high-quality journalism in the aerospace and defence sectors, earning a well-deserved reputation as Asia's largest media house in this domain. I wish SP Guide Publications continued success in its pursuit of excellence.

The cargo industry witnessed good yields during the pandemic, however, demand fluctuations are anticipated ahead and structural shifts are required for industry’s scaling

Given the highly interesting journey that air cargo has had during and after the pandemic, across the globe, its growth and structural transition are among the most anticipated talked about subjects. India’s air cargo industry also witnessed an interesting shift as the demand arose.

During COVID times, cargo proved to be the savior that was responsible for the survival of much of the industry. Despite serious capacity constraints, the remarkable strength of yields meant that cargo revenue quickly returned to, and in many cases exceeded, pre-COVID levels. The performance of air cargo during the pandemic upheld it as of critical strategic importance to airlines, especially in India. All major operators saw strong contribution from cargo:

However, prior to COVID, air cargo was largely considered to be non-strategic by Indian airlines especially in the domestic market. The domestic express market largely revolved around Blue Dart, operating just five freighters pre-COVID, highlighted Kapil Kaul in a CAPA India session. He brought in limelight the attempts to launch other dedicated cargo and express airlines which quickly failed in India. Despite several serious attempts including inter-ministerial efforts to remove structural barriers, cargo remained non-strategic to most. Only perhaps airports, freight forwarders and the supply chain were interested in cargo, but overall outcomes remained sub-optimal.

The key reasons for failure to realise the full potential from cargo operations as highlighted in the session included:

However, India’s dedicated freighter fleet has increased from 5 to 28 in last few years particularly last two as cargo has now become a boardroom agenda item. After COVID-19 though, the new found strategic importance of cargo was reflected in:

CARGO IN INDIA DURING PANDEMIC

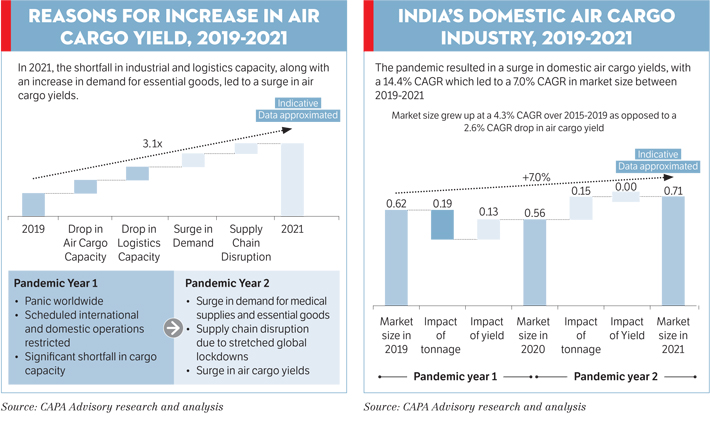

India faced a significant capacity drop relative to demand during pandemic. This led to an increase in cargo load factors in line with the global air cargo trend. In 2021, the shortfall in industrial and logistics capacity, along with an increase in demand for essential goods, led to a surge in air cargo yields.

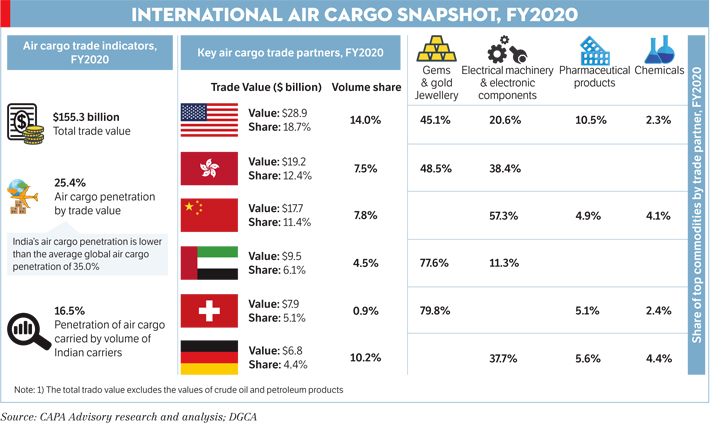

India witnessed stable trade during the pandemic and did not see any significant change in its air export and import trade baskets. India is a leading pharmaceutical exporter, with a 20 per cent share of the global supply based on volume catering to about 40 per cent of generic demand in the US and 25 per cent of all medicine demand in the UK. However, India’s pre-COVID supply chain for pharma and electronic sectors shows China as a high concentration zone, indicating risk for procurement. India is primarily dependent on China for key raw materials and components supplies for manufacturing electronic products. The other key suppliers are Hong Kong, Taiwan, and South Korea. China accounted for 37 per cent of the overall imports of India before COVID-19. COVID broke global value chains creating industry-wide disruptions. India’s heavy reliance on China for imports led to exposure to supply shocks during the pandemic.

The pandemic resulted in a surge in international air cargo yields, which increased 3.3 times in 2021 from the 2019 level, which led to the market increasing 76.2 per cent CAGR (compound annual growth rate) over 2019-2021. The pandemic also resulted in a surge in domestic air cargo yields, with a 14.4 per cent CAGR which led to a 7 per cent CAGR in market size between 2019-2021.

OPPORTUNITY FOR INDIAN CARGO

Pricing inefficiencies, operational bottlenecks and a relatively low penetration of technology in air cargo had rendered India somewhat uncompetitive against global peers. However, going ahead, there is a significant opportunity in cargo, especially on international routes as Indian carriers only capture around 10 per cent of international cargo to and from India (12 from India) 90 per cent is carried by foreign airlines. India’s leading passenger markets also align with many of its largest trade partners. In markets such as the US, Canada, UK and Australia; India has a surplus in trade volumes. Airlines can build long hall connectivity to core markets with the support of cargo which can significantly strengthen route economics.

According to CAPA Advisory, even in the domestic market significant opportunities exist and those airlines that invest in understanding the market in terms of industries commodities distribution and marketing-supported by integrated partnerships will benefit.

POSSIBLE DEMAND SUPPRESSION

Although many factors contributed to surge in yields for India’s air cargo business, CAPA suggests that this still is a temporary glitch majorly due to pandemic.

Air cargo yields will stabilise in the coming quarters, primarily due toan increase in capacity and the stabilisation of demand. In this regard CAPA identified some deflationary factors and some inflationary factors.

Deflationary factors include:

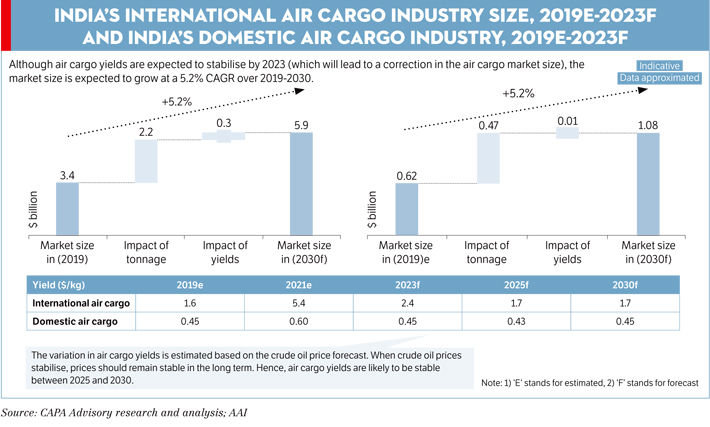

Although these factors will place upward pressure on air cargo yields, inflation will weaken demand further, which will, in turn, force carriers to reduce freight rates. Despite the expected growth in cargo throughout, the value of India’s international air cargo market will decline relative to the pandemic due to the normalisation of yields. CAPA believes that the market size which soared to about 10.5 billion by 2021 should start stabilising soon and there should be a correction and it should be about 5.4 billion by 2023. The very high air cargo yields that everyone earned during the two years of COVID should start stabilising soon and because of stabilistaion increase, the market size between 2021 and 2030 should drop by about 6.2 per cent CAGR.

The high cargo revenue growth achieved by many airlines, especially Indian carriers, despite a decline in the overall cargo tonnage, was due to surge in yields. This surge was largely due to the dual impact of supply constraints and an increase in demand due to a shift in the consumption basket. Although these factors helped carriers earn higher revenue and profits from the cargo segment, they are temporary. It is unlikely that these shifts and constraints are structural due to the following reasons:

FUTURE OF CARGO IN INDIA

However, there is still an opportunity for Indian carriers to expand their footprint in the air cargo industry, by fixing structural imbalances and by focusing on markets with high potential for passenger and cargo revenues. Although it must be noted that many of these markets are long-haul and only a few Indian carriers will be in a position to seize this opportunity.

The emphasis that Airlines are now placing on cargo is a fundamental shift and will alternately be a positive for the aviation industry and for the Indian economy. Realisation of the cargo potential is a mindset shift but on ground the structural shift will take time. Structural shifts in underlying demanddriven by the governments serious to teaching focus on make in India, trade competitiveness, re drawing of FTAs, PLI schemewill occur but over a period of time.

Many structural shifts are required to provide a muchneeded boost to the air cargo industry in India including:

(The article content is based upon CAPA India’s research shared during a webinar organisedby the advisory.)